hindsight2020

Final Approach

- Joined

- Apr 3, 2010

- Messages

- 6,733

- Display Name

Display name:

hindsight2020

Because they / know the rules and decided to ignore them. It's not brain surgery, if you assume the higher risk because someone sells you a bill of goods, promising things that they can't deliver, without you verifying first you will likely pay the piper.

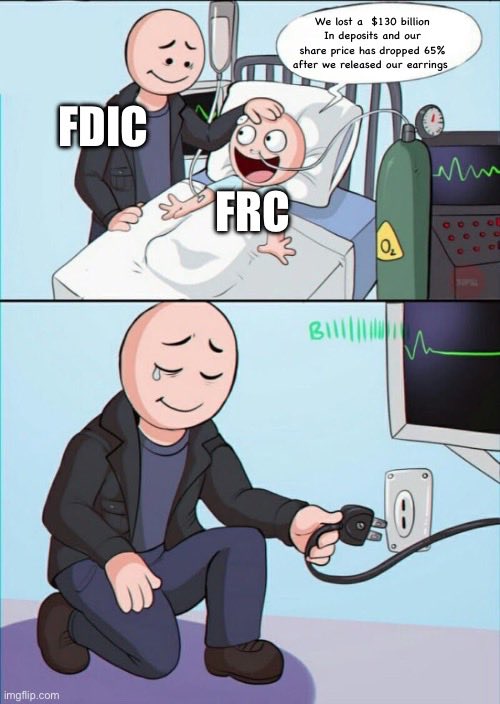

First Republic is still not out of the woods. They announced Friday they’ll suspend pay dividends on the preferred stock in addition to the already suspended dividends for common stock.

The stock’s value is down 90%; not sure they’ll make it to the end of the year.

And as of today...

And as of today...

My dad's house flooded last year. The people the insurance company hired to clean up unplugged a freezer full of game meat in the garage....so they could charge a phone. We were in New Mexico when I had the thought to have my sister make sure the breaker or GFI didn't pop. Breaker was good. But they left the phone charger behind. Contents had thawed and started dripping.Off-topic, but I predict that's roughly how I'm going to go out. I'll be in the hospital on some kind of machine, the cleaning person will come in, unplug the machine, plug in the vacuum, and I'll flat-line. Probably have had that nightmare because I've had cleaning people unplug ups's for servers to plug in cleaning equipment.

And now, after a month of hospice, FRC is gone.

To answer that question I'd be looking heavily at the institutions that funded CRE developments or acquisitions in SF/NY/... Particularly offices and retail. There's pain under the surface there even if no one is willing to admit it yet.Big question is who's next, if anyone..

I guess I should dig around my co's 10K and see what's what...To answer that question I'd be looking heavily at the institutions that funded CRE developments or acquisitions in SF/NY/... Particularly offices and retail. There's pain under the surface there even if no one is willing to admit it yet.

There's good reason to believe that lot of the banks and PE funds are still marking-to-make-believe on those assets. For evidence I submit to the jury Exhibit A: the bidding of 350 California St in SF this week that was what... 75-80% below it's value a few years ago? IDK how many institutions can properly afford to absorb those markdowns. Exhibit B would be Blackstone's BREIT having to put up the exodus gate 6 months in a row (yet still somehow new money does find its way in there, I have no idea why).

EDIT: And I recall seeing a headline about Brookfield also choosing to default on some properties recently too. The wave there is still in its early innings.

One of the conversations we’re hearing in the HR space is no backfill for attrition and new job offers contingent on in-office work.… institutions that funded CRE developments or acquisitions in SF/NY/....

That's interesting. Is that at the banks? Or just broadly across sectors?One of the conversations we’re hearing in the HR space is no backfill for attrition and new job offers contingent on in-office work.

I'm not a real estate expert by any means, so I was surprised to hear what it costs to do one of those conversions (for office towers -> residential at least). It sounds like many of these buildings would have to sell for 0$ (or less) in order to make that even remotely economical. And even with a conversion many of the buildings would not be attractive living spaces (e.g., lack balconies, insufficient sunlight, etc). Though I'd be curious to hear from an authoritative source on what the likelihood of that is.I’m not in the commercial to residential conversion industry, but I see that as a potential opportunity

WeWork... Another disaster brought to you by... *doesn't even need to check notes* ... Softbank!WeWork was absorbing excess Class A space at a discount and that venture failed spectacularly.

. When I first heard of WeWork in 2014 I actually thought it was a cool idea. It wasn't until late 2015 when I visited our company's office in London that I stopped by the WeWork office next door at Moorgate (a friend was working out of there). I remember being like "wow, this building is insanely nice, and this neighborhood is insanely nice, and how the hell can you afford to offer this space to customers with free beer, gourmet coffee, pizza, WeWork sponsored parties, and other amenities for 99$/month?". Oh that's right, you can't. At least not once Softbank's money cannon runs out. And that's why WeWork is trading at 40 cents on the dollar. EDIT ADDITION: and last I heard they have something like >40$ billion in lease liabilities. Good luck to landlords for collecting on that once they go tango uniform.

. When I first heard of WeWork in 2014 I actually thought it was a cool idea. It wasn't until late 2015 when I visited our company's office in London that I stopped by the WeWork office next door at Moorgate (a friend was working out of there). I remember being like "wow, this building is insanely nice, and this neighborhood is insanely nice, and how the hell can you afford to offer this space to customers with free beer, gourmet coffee, pizza, WeWork sponsored parties, and other amenities for 99$/month?". Oh that's right, you can't. At least not once Softbank's money cannon runs out. And that's why WeWork is trading at 40 cents on the dollar. EDIT ADDITION: and last I heard they have something like >40$ billion in lease liabilities. Good luck to landlords for collecting on that once they go tango uniform.That was a fantastic show and I binge watched it years ago. I just never considered that it could accurately portray real life. But that whole perspective changed when Softbank came along and gave hundreds of millions (or more) to anyone with anything resembling an idea.If you guys ever seen the HBO show Silicon Valley, It's a wonderful caricature of how inane that space can be

Every time I see that name or think of it, @denverpilot comes to mind. Even back then, he called that spade a spade.…Softbank...

I don’t do facebook.

Each episode was a gem indeed. Mike Judge has a talent for thisThat was a fantastic show and I binge watched it years ago. I just never considered that it could accurately portray real life. But that whole perspective changed when Softbank came along and gave hundreds of millions (or more) to anyone with anything resembling an idea.

If I was an investor in Softbank's vision fund and I saw them handing out money to companies like WeWork (who used the money for things like buying a pool wavemaking company) I would have fought to get my money back more aggressively than in Silicon Valley when Erlich attacked the kid on Richard's behalf for taking his money and not delivering his Aderall. Quite possibly my favorite (and unexpected) scene from that series.

There's both good and bad on Facebook, just like any site that relies on user-provided content. My main beef with it is the clunky user interface.You just gained some points on the respect-o-meter ...

I'm not a real estate expert by any means, so I was surprised to hear what it costs to do one of those conversions (for office towers -> residential at least). It sounds like many of these buildings would have to sell for 0$ (or less) in order to make that even remotely economical. And even with a conversion many of the buildings would not be attractive living spaces (e.g., lack balconies, insufficient sunlight, etc). Though I'd be curious to hear from an authoritative source on what the likelihood of that is.

Ok did I some research. And by I, I meant Morgan Stanley…I guess I should dig around my co's 10K and see what's what...